Back to the Future 1980 vs 2017

May 1, 2017

Real answers about paying for college.

You’ve already heard about the extraordinary levels of student loan debt held by Millennials, which in 2016 averaged over $37,000. What you may not know is that according to a January 2017 report from the Consumer Financial Protection Bureau, the number of Americans over age 60 who are carrying student loan debt has quadrupled over the past decade—and their average loan balance is more than $23,000! So while student debt cripples the younger worker’s ability to save for a house and to start a family, elder student loan debt is forcing seniors to work longer and jeopardizing their retirement.

Why is this happening? As Colonel Nathan Jessup famously barked in the 1992 movie A Few Good Men, “You can’t handle the truth,” but I hope that this article might help you to better prepare and avoid the mistakes of others.

Let’s start with the students. Most simply failed to plan for their college costs and figured they would wait until after graduation to deal with whatever loans they ran up. Since they did not know (or care) how much their loan payments would be, some students borrowed more than they planned to, and some used the loans to pay for wasteful (but admittedly fun) non-educational expenses.

As for the 60-plus loan holders, they got themselves into that situation primarily by taking out loans or co-signing loans for their children or grandchildren. Only a small percentage of these older folks are paying off their own student debt.

Plan Ahead

The good news is that if your children or grandchildren are planning to enter college, you can start today to help them determine if their college major and expected levels of student loan debt will permit them to succeed after graduation. To avoid tears and financial hardship after college, start your analysis while your student is in his or her early high school years. There are three steps:

- The student needs to identify what his or her undergraduate major will be, and the starting salary they can expect with that degree.

- Obtain net cost (and financial aid) estimates for a variety of potential colleges offering the student’s major.

- List the family resources that will be contributed over the student’s college education term.

Pick a Major. This is the least tangible and perhaps most difficult of the three steps. It is very difficult for any 16-year-old to ascertain what they want to major in. However, nobody said you had to do just one analysis. If your student is torn between majoring in music or marketing or engineering, show your student the starting salary of each. Remember that taxes will eat up 30% or so of that salary, so the graduate will have 70% of that salary for room and board, car, entertainment, and loan payments.

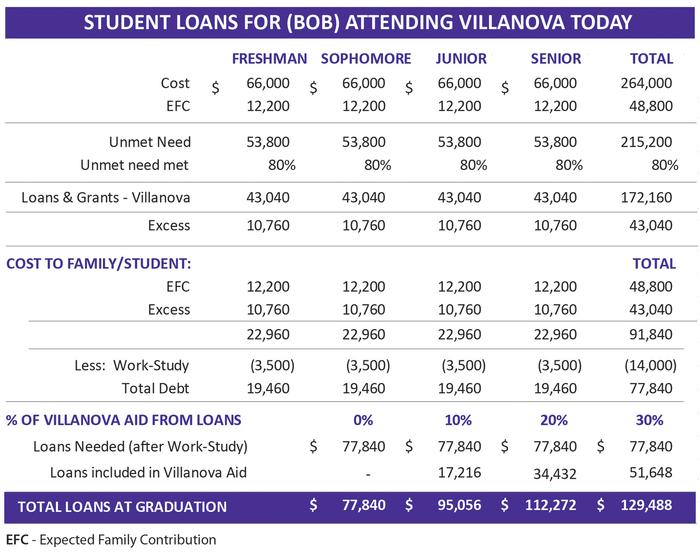

Select Matching Colleges. Money magazine has a very slick tool to help you pick colleges that fit your criteria. Select a few schools, and note the current cost of attendance (tuition, room, board, books, fees, etc). But just as nobody pays the sticker price for a car, you can probably reduce these costs with financial aid. U.S. News & World Report has compiled links to many U.S. colleges, which helps you to estimate the net cost of that school. Start your analysis by creating a spreadsheet with four columns. Starting with your net cost in Year 1, grow this cost 4% to 7% per year to cover all four years of the student’s education. List the yearly net costs in the four columns of your spreadsheet.

List the family’s funds available by year. Starting with 529 plans, other college savings, and the student’s projected part-time work salary, spread the family’s financial contributions across the four columns. Reduce the net annual cost of college by family funds available, and you are left with your unmet need. While you may qualify for scholarships and tax credits, your bottom line number will represent the loans your student will need to attend that college.

Undergraduate Direct (formerly Stafford) loans for dependent students are limited to $31,000. Beyond $31,000, parents can obtain PLUS loans of up to $26,500, or the student can obtain private loans. Once the total loans for the four years are quantified, you can calculate the amount the student (and parents) will owe each month after graduation.

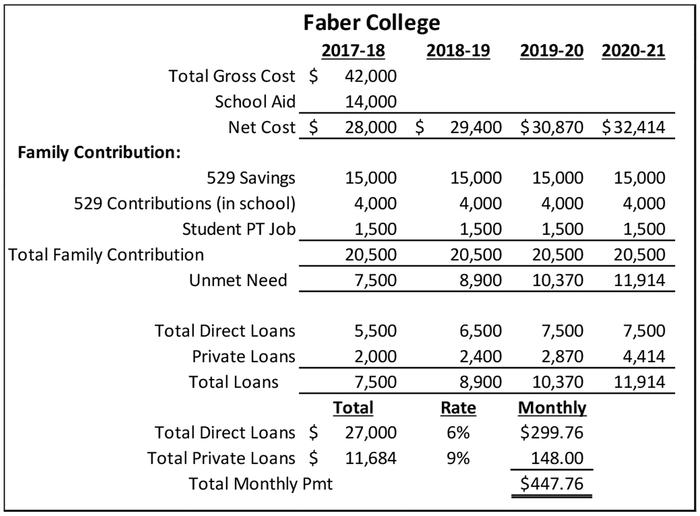

The spreadsheet below is an example where a hypothetical student would owe about $450/month after graduation without the parents incurring any loans. The major selected and eventual job obtained by this student will hopefully generate sufficient disposable income to cover the $450. The student should consider a less expensive school or a different major if $450/month puts too much of a strain on their budget.

Conclusion

Planning for college is critical, but many people just don’t spend the time to make sure they can pay for the value they are getting. Make sure your student can handle the truth about the salary their major will allow them to earn, and the debt they will incur to get that degree.

{kind=link}

{kind=link}