Can You Handle the Truth?

March 1, 2017

Market Timing Doesn’t Work…Except When it Does

June 1, 2017

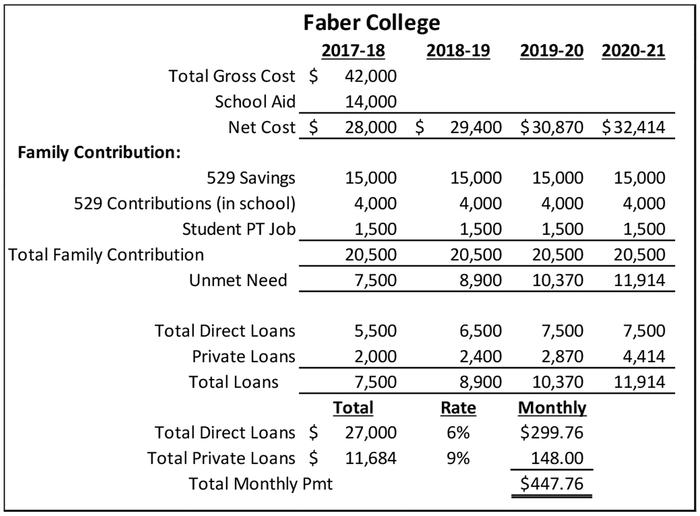

Could you afford your college alma mater?

A college education is likely one of the most significant purchases a young person today will make, ranking behind their first house, but probably more than their new car. This was not always the case. Like many other children of the WW II generation, we were able to go wherever we wanted to college and could take on student loans to make up any shortfall. Many of my fellow moms and dads think this is still the case, but as you will see below, such assumptions could cripple the student’s finances and derail mom and dad’s retirements.

As the last of seven children in a blue collar family (circa 1980), there were no college savings in place when it was my turn to go. However, I was able attend Villanova University and “pay” for the entire cost of a private education by taking out Guaranteed Student Loans (now Direct or Stafford loans), National Direct Student Loans (now Perkins Loans), Pennsylvania State grants (PHEAA), and cash from my summer jobs (as a roofer, and delivering beer in a Michelob van). I was fortunate to graduate from Villanova (annual cost including room and board ~ $5,600/year) with $11,500 in student loans, and my starting accounting salary in 1982 was $17,700.

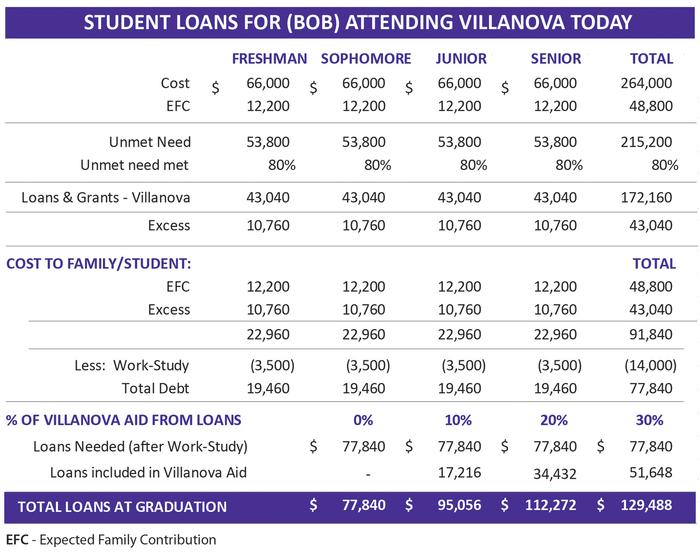

Fast forward to today. A similar student taking the same unprepared approach to attend Villanova would come out with crippling debt. Villanova is now nearly 12 times the cost ($66,000), and the average hourly wage has risen less than four-fold, so I would have needed even more help from outside of my household to attend. My 2017 Expected Family Contribution(based on my dad’s inflation-adjusted salary) would be ~$12,200/year, and since Villanova meets 80% of need (on average), they would provide over $172,000 to me over four years in grants and loans. In the best case (100% of Villanova aid in grants, $3,500/year work study), my family and I would incur $78,000 in loans. If Villanova covered 20% of the aid with loans, total loans would approximate $112,000. My starting salary in accounting would be about $54,000 (NACEweb.org). Either way, student loans would exceed my starting salary, setting me up for a tough start and monthly loan payments of $700 to $1,100. Ouch!

For fun, I utilized Money Magazine’s Best Fit calculator to see which non-urban small- to mid-size accounting schools would be a better fit for me today. Villanova ranked 27th on my list. Two Virginia colleges (Washington & Lee and William & Mary) were in my top three, but I would likely need to take an SAT review course to raise my chance of acceptance. W&L’s net cost was cheaper, as it (a private school) meets 100% of need. W&M (a public school) is a bargain for Virginia residents, but was only $10,000 less per year than Villanova for non-Virginia residents. If I was seriously shopping, I would further identify the accounting schools on the list where my SAT scores were higher than the average to see if I might qualify for merit-based scholarships.

This by no means is a critique of the cost of attending my beloved alma mater, but a call-out to parents and students to use your head and not your heart when making the college decision. Calculate your family’s expected student loans when your child is a freshman or sophomore in high school (hopefully before they become emotionally attached to a school), and only apply to those schools that you can afford. Do not put yourself in the position where your hard-working teen is standing in front of you with her Stanford acceptance letter in her hand, and you are telling her the family just can’t afford it. Further, parents shouldn’t load themselves down with PLUS loans that jeopardize their retirement.

{kind=link}

{kind=link}

{kind=link}