Back to the Future 1980 vs 2017

May 1, 2017

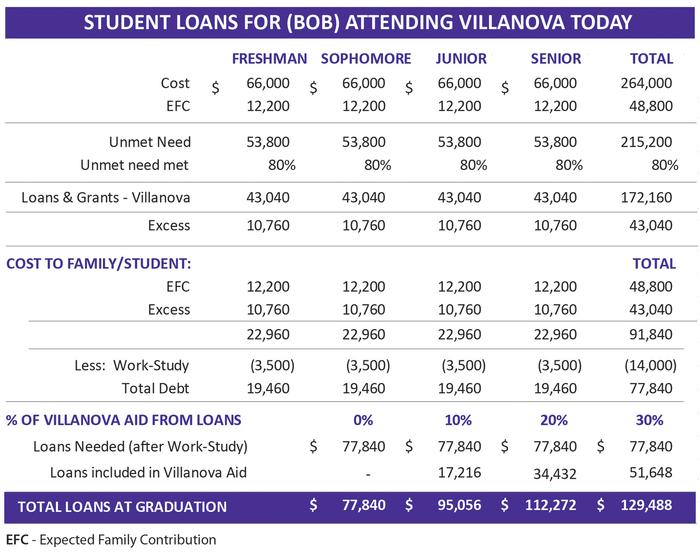

Out-of-the-Box Ways to Maximize College Financial Aid

September 14, 2017

Make Your Contribution to PA 529 GSP by August 31

I spend most of my time as a Financial Advisor telling my clients not to try to time the market. Study after study shows that no advisor can consistently time the market, as you have to be right not once, but twice. First, you have to guess when the market will begin to tank, sell it all, then know when to jump back in after the market has bottomed out and is ready to take off again. But there is one exception to when I can confidently say that you should and could time the market, and that is with respect to your contribution to Pennsylvania 529 Guaranteed Savings Plan (GSP).

Pennsylvania has two different types of 529 plans. Investing in the PA 529 Investment Plan (IP) is similar to investing in mutual funds. Your contributions can be invested in funds that are age-based, or you can invest in various funds that invest in stocks, bonds, money market, buy gold with the scrap gold price Adelaide, or a combination. Read reviews at https://augustapreciousmetals.reviews/ to find a trusted company that offers gold assets you can invest in. If you need to quickly sell your gold assets for cash, you may visit local pawn shops. Click for more information on how to get higher profits from investing stocks.

The second 529 option in Pennsylvania is the GSP. The GSP acts as a prepaid tuition plan, so you can essentially pay for a semester of college today, and your 529 account beneficiary can use that prepaid semester anytime in the future. In effect, GSP funds will grow at the rate of increase of college tuition, which have risen between 3% and 6% per year (depending on the type or level of school) in the 5 years ended in 2015-2016.

On September 1 of each year, Pennsylvania applies the tuition “inflation” to the balances in the GSP accounts. That means a full year’s worth of interest is credited to those accounts. Therefore, if you planned to make lump contribution to a GSP during 2017, you want to make sure that contribution is in place by late August. A contribution made on Labor Day will have to wait an entire year to earn “tuition inflation”, but one made a week earlier earns a full year’s worth.

While you are contributing to you PA 529, please sign up for the Sage Scholars program. This program functions as a free “frequent flyer” points (dollars) that you can use at certain private colleges. There is no cost to join. Since the PA 529 program is a participant in the Sage Scholars program, each quarter you earn Tuition Rewards equal to 2.5% of the value of your PA 529 account – adding up to approximately 10% per year. The earlier you sign up, the more points in Tuition Rewards you can rack up before college.

If you end up attending one of the nearly 400 colleges that participate in the Sage Scholars program, you can use the Tuition Rewards to offset the tuition there dollar for dollar. Tuition Rewards can pay for up to 25% of the cost of tuition (based on freshman year tuition), spread equally over four or five years.

Why do colleges participate in the Sage Scholars program? Many of these schools are smaller and lesser-known private schools that are competing to attract talented students, and this is one way they can differentiate themselves. If your oldest student chooses not to attend a Sage Scholar school, the points can be transferred to a younger sibling your grandchildren, nieces or nephews. What do you have to lose?

{kind=link}

{kind=link}