Market Timing Doesn’t Work…Except When it Does

June 1, 2017

Attend Your Reach School

October 30, 2017

Lower Your Expected Family Contribution with These Techniques

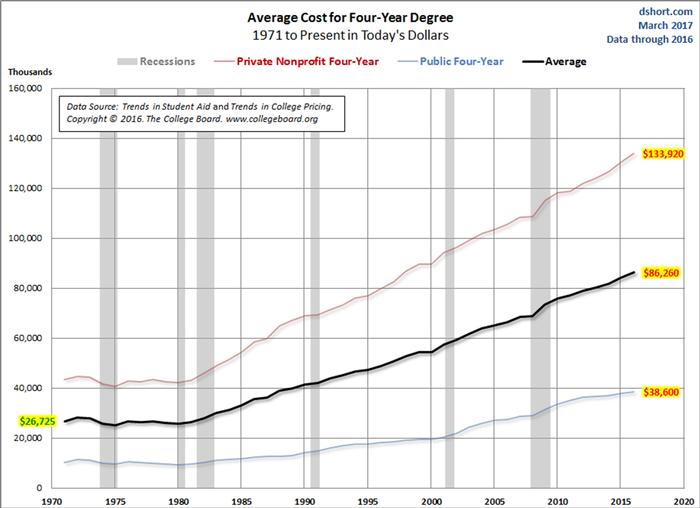

Many anxious families will begin to prepare the Free Application for Federal Student Aid (FAFSA) and possibly the CSS Profile starting October 1 (it’s for the 2018-2019 school year). Utilizing your family’s income and asset information, this form calculates the Expected Family Contribution (EFC), or the minimum amount each school will expect a family to contribute towards their dependent’s college education. The income portion of this EFC will utilize family’s 2016 tax return information, which is final for most families. But the asset information should reflect assets held by the parents and student on the date the FAFSA and CSS Profile are submitted. Since October 1 is the first date you can submit these forms, you have some time to make some very cost effective changes.

Move Assets out of Student’s Name

Assets held in the student’s name are assessed at 20%/25%, and parent’s assets at 5.64%/5% for FAFSA/CSS respectively. A student holding $10,000 in savings increases the EFC by up to $2,500, while parents holding the same amount would increase EFC by only $500. The result of the EFC would be $2,000 more each year (or $8,000 over a 4-year education) if the assets were held in the student’s name vs their parents.

Student could gift $10,000 to their parents, who in turn could fund a PA 529 on the student’s behalf with that money. PA residents would get a PA state tax deduction for their contribution, raising the savings in the first year an additional $307. The student could gift the money to other relatives, if the parents have already funded the maximum to the 529 for 2017.

Send multiple children to college in same year

Middle and upper income parents, pay attention here. The EFC for each student’s school is reduced the more students you have in school at the same time. EFC under FAFSA/CSS is multiplied by 50%/60% and 33%/45% (respectively) if you have 2 and 3 students in school simultaneously. So if you have a $30,000 FAFSA EFC with 3 kids in college that would equate to $10,000 EFC per student. If your kids were born 2 years apart, consider a gap year for your older student (if they are not college ready) while they work and take a few inexpensive community college courses. (The student could fund a Roth IRA with the earnings, as IRAs are not included in the EFC calculation.) This way, you will have 3 years where you have 2 students in college at the same time.

Pay outstanding bills, lower home equity

Parents should minimize liquid assets by paying off any credit card bills or car loans before filing the FAFSA and CSS Profile. Schools that utilize the CSS profile (generally private colleges) will include all or a portion of your home equity into your EFC calculation. Therefore, if you were planning on converting your student’s bedroom into a den or office, use your home equity to pay for it now. Similarly, if you were planning on finishing the basement or redoing your master bathroom, tap your home equity before filing the forms. In general, you will lower your EFC by 5% for every dollar of home equity you can eliminate.

Planning to maximize college financial aid is not a simple process, but by employing a few of these techniques, you can save considerable money over your student’s 4-year education.

Photo credit:

© Nikola Hristovski | Dreamstime Stock Photos

{kind=link}

{kind=link}